2019-11-01

In this post I introduce a class of discrete stochastic volatility models using a nice notation and go over some special cases including GARCH and ARCH models. I show how to simulate these processes and how parameter estimation performs. The Python code I wrote for these experiments is referenced at the end of the post.

If you are not that familiar with the probability theory, do yourself a favor and just read over the mathematical intricacies, or maybe skip right ahead to the “special cases” section and pick the details from here only of they seem relevant to you.

\global\def\Xpred#1{(X_s)_{s\lt #1}}

Let \left( \Omega, \mathcal A, \mathcal F, P \right) be a stochastic basis with a complete \sigma-algebra \mathcal A of measurable subsets of \Omega, a probability measure P, and a filtration \mathcal F = (\mathcal F_t)_{t=0, 1, \ldots}.

Thus, the time instances are indexed using non-negative integers 0, 1, \ldots.

To get the first t elements of a sequence X = (X_0, X_1, \ldots), I use the notation \Xpred{t} = (X_0,\ldots,X_{t-1}).

A discrete stochastic volatility (DSV) model X = (X_0, X_1, \ldots) is a real-valued stochastic process (a sequence of random variables) satisfying the following equations:

\begin{aligned} X_t &= \mu_t + \sigma_t Z_t \\ \mu_t &= \phi_0 + \sum_{i=1}^{p} \phi_i f_i (\Xpred{t}) \\ \sigma_t^2 &= \gamma_0 + \sum_{i=1}^q \gamma_i g_i(\Xpred{t}) + \sum_{i=1}^r \lambda_i h_i((\sigma_s^2)_{s\lt t}). \end{aligned}

Ingredients:

To formulate the specializations of the general DSV model the following notation comes in handy.

The backward shift operator B^j, for j\geq 0, produces a delayed version of its argument process, i.e. B^j (X)_t = X_{t-j}, if t-j \geq 0, and B^j (X)_t = 0, if t-j \lt 0. For example

B^1(X) = B(X) = (0, X_1, X_2, \ldots).

For convenience, I set B^1 = B and B^j_t (X) = B^j(X)_t = X_{t-j}.

For all the special cases in the list below, I assume that the functions f_i, g_i, and h_i pick a single element from the history of the argument process, i.e. f_i = h_i = B^i_t, and g_i(\Xpred{t}) = B^j_t(X^2).

GARCH process definitions found in textbooks additionally set \mu\equiv 0.

The GARCH(1, 1) processes are quite popular, so let’s stat the dynamics explicitly:

\begin{aligned} X_t &= \sigma_t Z_t \\ \sigma_t^2 &= \gamma_0 + \gamma_1 B_t(X^2) + \lambda_1 B_t(\sigma^2). \end{aligned}

In an ARCH process, the volatility has the simplified form with \lambda_i = 0 for all i, and \mu \equiv 0.

\begin{aligned} X_t &= \sigma_t Z_t \\ \sigma_t^2 &= \gamma_0 + \sum_{i=1}^q \gamma_i B^i_t(X^2). \end{aligned}

An ARCH(1) process additionally satisfies \gamma_i = 0 for all i \geq 2:

\begin{aligned} X_t &= \sigma_t Z_t \\ \sigma_t^2 &= \gamma_0 + \gamma_1 B_t(X^2). \end{aligned}

Discrete stochastic volatility models are typically used to model the log-returns of an observed time-series. Therefore in order to simulate a path of the original time-series we need to simulate its log-returns and calculate Y = Y_0 \prod_{s=0}^t \exp(X_s).

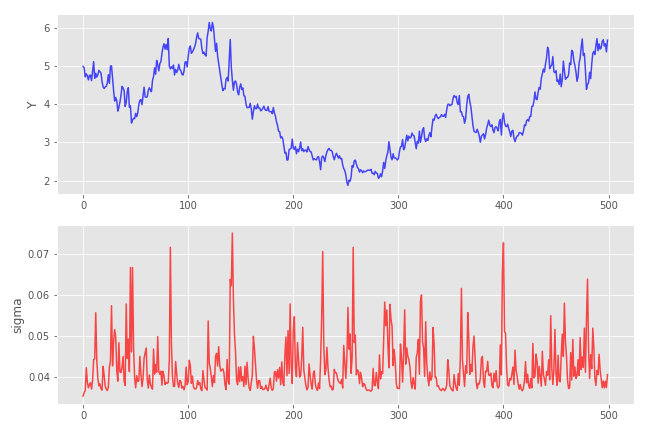

A sample path of a GARCH(1,1) process driven by the Gaussian noise with parameters (\gamma_0, \gamma_1, \lambda_1) = (0.001, 0.2, 0.25):

Note that the \sigma process for t>0 cannot go below the level of \sqrt{\gamma_0 (1 + \lambda_1)} \approx 0.0353

Maximum-likelihood (ML) parameter estimation is the method of choice for all the discussed models since the transition density, i.e. the density of X_t given the past information \mathcal F_{t-1} is known explicitly. Log-likelihood function of the process sample path x is thus given by

\ln L(\theta; x) = \sum_{s=1}^t \ln \eta_Z \left( \frac{x_t - \mu_t(\theta)}{\sigma_t(\theta)} \right) - \ln \sigma_t(\theta),

where \theta = (\phi_i, \gamma_i, \lambda_i), and \eta_Z is the density of Z. Minimizing the above log-likelihood function yields the maximum-likelihood estimate \hat\theta for \theta:

\hat\theta(x) = \operatorname{argmin}_{\theta} \ln L(\theta; x).

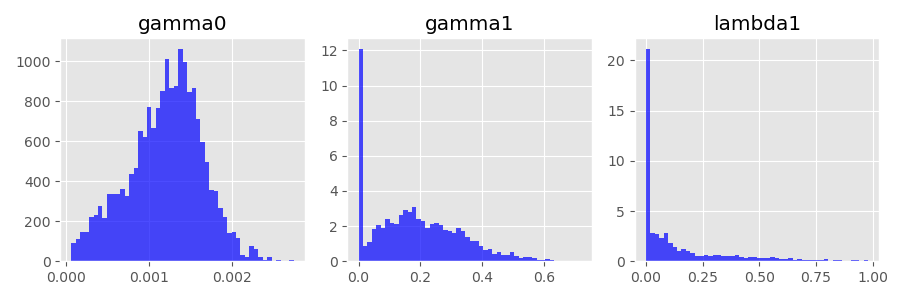

In order to test the ML parameter estimation procedure, I perform the following Monte-Carlo experiment.

As expected, the estimator \hat\theta is very inaccurate and, in most cases, doesn’t even come close to the true vector \theta. In particular, the estimated \gamma_1 and \lambda_1 are often set to zero (see the histograms below).

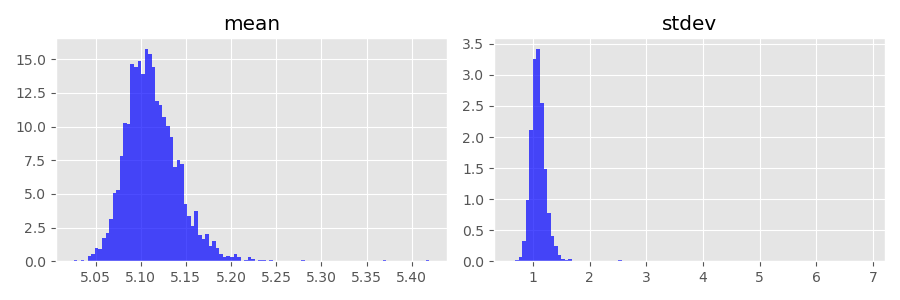

On the other hand, the process means and standard deviations coming from the estimated \hat\theta are much more accurate. This is a good thing, because we usually care more about recovering the characteristics of the unknown data generating process and not so much about the true parameter values of the model.

The noise process Z doesn’t have to be normalized to mean 0 and variance 1. In fact, we just need to make sure that the distribution of the random variable Z_t admits a density. If this is the case, both, process simulation and ML estimation work as described.

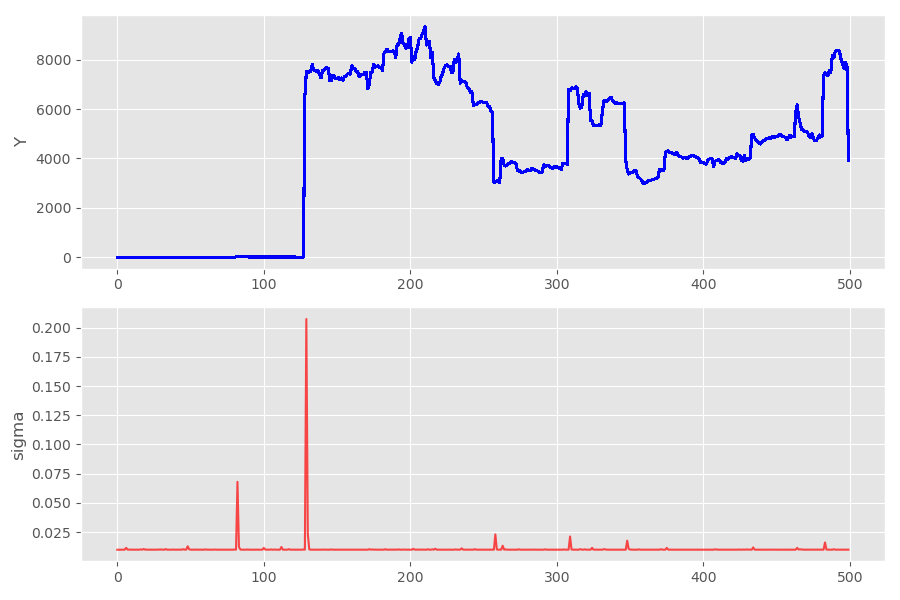

So how about replacing the Gaussian noise with a noise sampled from the Cauchy distribution? In many probability theory books, the Cauchy distribution is used a counterexample, because it has many “pathological” properties. For example, it has no mean and, consequently, no variance. (“No mean” means that the integral used to define the first moment diverges, i.e. has no finite value.)

This is the theory which I learned few years ago. What I didn’t know is how erratic samples from a Cauchy distribution look like. Just take a look at a sample path of the GARCH(1,1) process with the parameter vector (\gamma_0, \gamma_1, \lambda_1) = (0.0001, 0.001, 0.01):

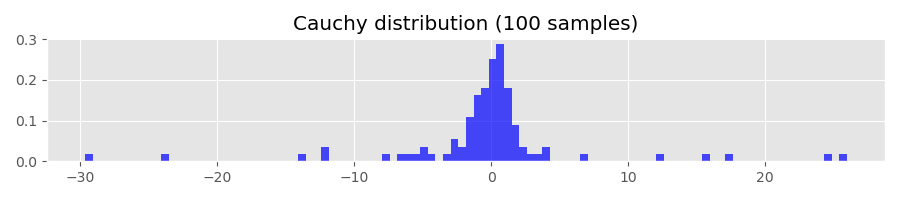

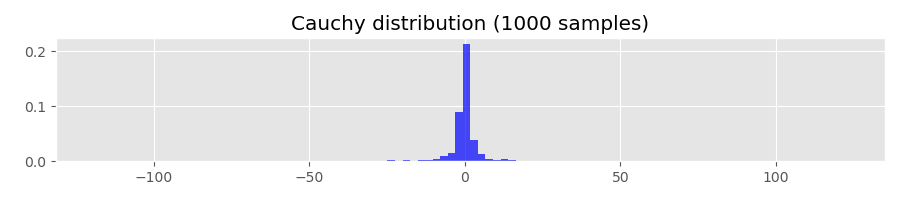

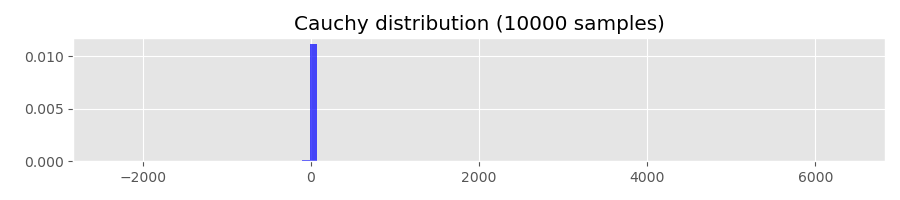

If you play around with the path generating function long enough, you may even generate a floating point overflow exception. The Python function I used to generate histograms shown above fails because of that. To see what is going on under the hood, let’s generate some histograms using samples from the Cauchy distribution:

The Cauchy distribution has the quantile function

Q(p) = \tan (\pi (p-0.5)).

Evaluating Q(1-p) for p=0.01, 0.001, 0.0001 gives

Q(0.99) ~= 31.82

Q(0.999) ~= 318.31

Q(0.9999) ~= 3183.10This means that, for example, with probability of 0.0001 the sampled values are greater than 3183.10. For comparison, let’s calculate the corresponding quantiles of the standard normal distribution:

> from scipy.stats import norm

> print(norm.ppf(0.99))

2.32

> print(norm.ppf(0.999))

3.09

> print(norm.ppf(0.9999))

3.71